-

After Two Decades, the Cartier Women’s Initiative Is More Impactful Than Ever

After Two Decades, the Cartier Women’s Initiative Is More Impactful Than EverRooted in women’s empowerment and social impact, the program celebrated its 20th anniversary this June—with no signs of slowing down.

-

Prince Philip Said "Everything Crumbles" Without Work

Prince Philip Said "Everything Crumbles" Without Work"Harry had previously spoken to his grandfather about death..."

-

My Surreal Journey of Getting Fired by the Trump Administration

My Surreal Journey of Getting Fired by the Trump AdministrationEmily Loker had a PhD, a condo, and a five-year plan as a federal employee. Then her job was eliminated.

-

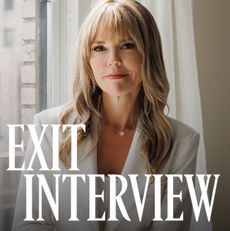

Wendy McMahon Isn’t Done Making News

Wendy McMahon Isn’t Done Making NewsThe former CBS News chief opens up about her sudden departure from one of legacy media’s top positions.

-

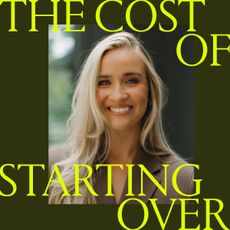

I’m a Money Expert—and I Lost Nearly $100,000 to the Man I Was Supposed to Marry

I’m a Money Expert—and I Lost Nearly $100,000 to the Man I Was Supposed to MarryIn the first installment of The Cost of Starting Over, money expert Chloe Elise reveals how financial infidelity derailed her life—and what it took to reclaim it.

-

The Witches of Wall Street

The Witches of Wall StreetA new generation of women is blending mysticism with money management—and rewriting the rules of getting rich.

-

Coach Sandy Brondello Breaks Her Silence on the Offers She Turned Down for Toronto

Coach Sandy Brondello Breaks Her Silence on the Offers She Turned Down for TorontoThe WNBA history-maker sets the record straight on the whirlwind between her Liberty exit and her fresh start with the Toronto Tempo.

-

Abby Phillip Wasn’t Looking for the Spotlight. She Earned It Anyway.

Abby Phillip Wasn’t Looking for the Spotlight. She Earned It Anyway.After writing her first book on Jesse Jackson’s legacy, the CNN anchor reflects on risk, resilience, and staying true to herself.

-

How to Recognize When It's Time to Pivot in Your Career

How to Recognize When It's Time to Pivot in Your CareerSponsor Content Created With Marshalls

Three female founders weigh in on the power of making a pivot.

-

5 Smart Money Moves For Financial Security

5 Smart Money Moves For Financial SecuritySponsor Content Created With Marshalls

Top insights from author and finance expert Erin Lowry during Power Play Philadelphia.

-

How to Define Your Own Direction With Confidence

How to Define Your Own Direction With ConfidenceSponsor Content Created With Marshalls

An inside look at day two of Power Play.

-

Melinda French Gates Knows Exactly How Her Career Ends

Melinda French Gates Knows Exactly How Her Career EndsOne year since the philanthropist left the Gates Foundation, she’s still figuring things out—but there’s one cause she’s committed to for life.

-

How Marshalls Is Helping Women Access the Good Stuff in Life

How Marshalls Is Helping Women Access the Good Stuff in LifeSponsor Content Created With Marshalls

From in-person events to digital resources, women are gaining the support they need to create the lives they've always dreamed of.

-

How My Job’s ‘Wellness’ Program Nearly Sent Me Over the Edge

How My Job’s ‘Wellness’ Program Nearly Sent Me Over the EdgeI was grieving my mom while trying to survive a corporate wellness culture obsessed with positivity. It nearly broke me.

-

After Nearly 20 Years With Nike, Tania Flynn Walked Away to Build a New Legacy at Athleta

After Nearly 20 Years With Nike, Tania Flynn Walked Away to Build a New Legacy at AthletaWhile it was a difficult decision, taking a leap of faith was exactly what Flynn needed.

-

How a Shared Fertility Struggle Empowered Two Ex-Nike Employees to Launch Their Own Prenatal Company

How a Shared Fertility Struggle Empowered Two Ex-Nike Employees to Launch Their Own Prenatal CompanyAfter nearly two decades, Vida and Ronit parted ways with Nike and channeled their personal hardships into a new mission-driven venture.

-

Meet the Millennial Women Buying Their Own Engagement Rings

Meet the Millennial Women Buying Their Own Engagement RingsThere's nothing wrong with it. So why does it feel so uncomfortable?

-

They Got Everything They Wanted Professionally by 30. Then What?

They Got Everything They Wanted Professionally by 30. Then What?Reaching an all-time career high at a young age comes with a lot to celebrate—and a lot of pressure, too.

-

Are Millennials Secretly Rich?

Are Millennials Secretly Rich?New data claims the generation is wealthier than previously thought. But why doesn't it feel that way?

-

5 Steps to Money Mindfulness

5 Steps to Money MindfulnessSponsor Content Created With TD Bank

It's simpler than you think.

-

Work Wives Are Going Extinct

Work Wives Are Going ExtinctThey're becoming less common as remote and hybrid work get more prevalent. But is now the time when we need them the most?

-

Boredom Helped These Founders Build a Bathing Suit Brand

Boredom Helped These Founders Build a Bathing Suit BrandLaura Low Ah Kee and Shannon Savage left their executive roles to try something new.

-

What Will It Take to End Stay-At-Home Mom Shame?

What Will It Take to End Stay-At-Home Mom Shame?“Our culture around caregiving is ripe for reexamination.”

-

Former 'Marie Claire' Editors in Chief Reminisce About Their Time on the Job

Former 'Marie Claire' Editors in Chief Reminisce About Their Time on the JobIn honor of the magazine's 30th anniversary, we asked them to share favorite memories and what they learned while at the helm.

-

Ella Emhoff Never Intended to Be an It Girl—All She Wants Is to Knit

Ella Emhoff Never Intended to Be an It Girl—All She Wants Is to KnitThe second stepdaughter and former fashion model opens up about her true passions: art, knitting, and community.

-

3 Women on How They Unleashed Their Potential and Followed Their Professional Dreams

3 Women on How They Unleashed Their Potential and Followed Their Professional DreamsThese inspirational stories will have you ready to leap into your dream life.